Lubes em Foco Magazine – issue 97

Click on the magazine and read, download, or share the articles:

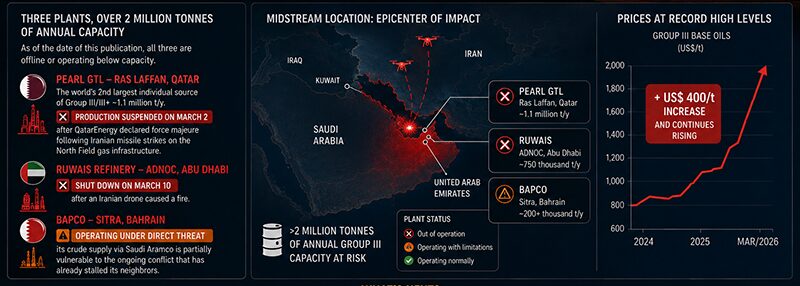

Three Group III plants in the Middle East account for more than 2 million tons of annual capacity. As of the date of this publication, all three are out of operation or have compromised operations. Pearl GTL, in Ras Laffan, Qatar — the world’s second-largest single source of Group III/III+, with ~1.1 million tons/year — suspended production on March 2 after QatarEnergy declared force majeure, a consequence of Iranian drone attacks on the gas infrastructure of the North Field. ADNOC’s Ruwais refinery in Abu Dhabi shut down on March 10 after an Iranian drone caused a fire. And BAPCO’s plant in Sitra, Bahrain — the region’s third-largest producer — operates under direct threat, with its crude oil supply via Saudi Aramco partially vulnerable to the same conflict that has already paralyzed its neighbors.

Three Group III plants in the Middle East account for more than 2 million tons of annual capacity. As of the date of this publication, all three are out of operation or have compromised operations. Pearl GTL, in Ras Laffan, Qatar — the world’s second-largest single source of Group III/III+, with ~1.1 million tons/year — suspended production on March 2 after QatarEnergy declared force majeure, a consequence of Iranian drone attacks on the gas infrastructure of the North Field. ADNOC’s Ruwais refinery in Abu Dhabi shut down on March 10 after an Iranian drone caused a fire. And BAPCO’s plant in Sitra, Bahrain — the region’s third-largest producer — operates under direct threat, with its crude oil supply via Saudi Aramco partially vulnerable to the same conflict that has already paralyzed its neighbors.

Added to this is the Chinese blockade of petroleum product exports, decreed on March 4 by the NDRC: China was not, in fact, a relevant escape valve for Group III — base oil export quotas were already very small before the conflict — but the blockade eliminates any residual possibility and further compresses the global availability of VGO and hydrocracking capacity.

This article maps, with data updated to March 16, 2026, the main global Group III manufacturers, their capabilities and operational status — and presents a structured analysis of what Brazilian policymakers should consider doing now and in the medium to long term.

Group III in Brazil: Small in volume, central in value.

Group III accounts for approximately 10% of the total volume of base oils consumed in Brazil — a number that underestimates its economic importance. It is precisely in the highest value-added segments of the lubricant industry that Group III is irreplaceable: synthetic and semi-synthetic engine oils for the light and commercial vehicle fleet, new generation automatic transmission fluids, high-performance industrial oils, and greases for demanding applications. In terms of revenue per ton, Group III is at the top of the pyramid of the mineral base oil mix — and it is precisely the input that enables the premiumization of the portfolio that the Brazilian market has been pursuing in recent years.

All Brazilian demand for Group III is met by imports. The country has no domestic production — there is not a single Group III plant in the national territory — and there is no project on the visible horizon to change this reality. In 2025, the main Group III suppliers to Brazil were South Korea (SK Enmove, S-Oil), Bahrain (BAPCO), Qatar (Shell Pearl GTL), and Malaysia (PETRONAS).

It is important to qualify the nature of the risk for each of these sources. Qatar and Bahrain are at the epicenter of the conflict, with plants physically paralyzed or compromised. Korean producers, in turn, do not suffer the risk of direct attack — but are subject to severe and increasing impacts on production and logistics costs, resulting from the rise in light Arab crude, the Hormuz blockade, the escalation of VGO, and maritime freight. These cost vectors affect, to varying degrees, all base oil production from groups I to III, and are the main channel through which the war reaches the Korean market.

This structural dependence was never perceived as a critical risk while global supply was functioning. The conflict of February-March 2026 changed this picture overnight.

The three Group III producers from the Middle East

Shell Pearl GTL — Ras Laffan, Qatar

Pearl GTL is the world’s second-largest single source of Group III/III+ gas: ~1.1 million tons/year of Group III+, produced via GTL conversion of natural gas from the North Field. It is a Shell/QatarEnergy joint venture, operational since 2011. Its entire process depends on a single input — gas from the North Field — with no alternative feedstock.

On March 2, Iranian drones attacked Qatari gas facilities. QatarEnergy declared force majeure and suspended all production. With no alternative feedstock, Pearl GTL ceased operations. The Qatari Energy Minister warned that the continuation of the conflict could force all Gulf exporters into force majeure — a consequence that, in his words, will ‘bring down the world’s economies’. There is no forecast for resumption.

ADNOC — Ruwais, Abu Dhabi, UAE

The Ruwais plant produces ~525,000 t/year of Group III/III+ (ADbase®) and ~100,000 t/year of Group II, integrated into the world’s fourth largest refinery (~922 kbd total refining capacity). JV: ADNOC 65%, Eni 20%, OMV 15%.

On March 10, an Iranian drone caused a fire and the refinery was shut down as a precaution. Abu Dhabi activated air defenses at least twice. Jebel Ali — the UAE’s primary export port — suffered infrastructure damage. Resumption indefinite.

BAPCO — Sitra, Bahrain

BAPCO operates a 400,000 t/year Group III (BAPbase®) plant in Sitra, with isodewaxing technology from Chevron Lummus Global. Feedstock: unconverted oil from the hydrocracker at the Sitra refinery, which relies on a pipeline from Saudi Aramco (~220,000 bpd of crude). BLBOC (Bahrain Lube Base Oil Company) is the affiliate that manages the plant.

Bahrain was directly attacked: explosions near Manama airport in the first week of March. BAPCO was not confirmed as a direct target, but its dependence on Saudi crude and the overall deterioration of security in the Gulf put the plant at a high operational vulnerability.

Nota: Luberef — Yanbu, Arábia Saudita

The Yanbu Growth II project, which would introduce approximately 300,000 tons/year of combined Group II and III crude oil, was in pre-commissioning in February 2026. The startup was suspended when the war began. Luberef remains a producer of only Group I and II crude oil—relevant here as capacity that was weeks away from becoming operational when the conflict broke out.

The cost cascade

The cascade of costs resulting from the war affects the entire base oil industry, from GI to GIII, and includes even geographically safe plants.

Crude and VGO

Brent crude crossed $100/barrel in the week of March 9th—a 43% increase from the pre-war level of approximately $70. VGO (vacuum gas oil) is the main feedstock for hydrocrackers producing Group GI, GII, and GIII base oils, and is sold at a premium over the price of crude oil. With Brent rising and light Arabian crude—the preferred input for the production of high-VI paraffinic base oils—becoming scarcer and more expensive, VGO prices are rising sharply. Korean refineries have no equivalent substitute for this specific crude.

Crack spread of diesel and middle distillates: the vector that puts pressure on VGO from the demand side

Crack spreads for diesel and jet fuel have exploded since the start of the conflict. European diesel futures rose 34% in the two days following the start of the attacks. The price of jet fuel in Singapore reached US$230/barrel—almost double that of Brent. The reason is structural: approximately 20% of global jet fuel exports and a significant portion of diesel transited the Strait of Hormuz, originating from Gulf refineries that are now paralyzed. The Middle East refinery complex—Sitra, Ruwais, and the Saudi and Iraqi refineries—was a central hub for exporting middle distillates to Europe and Asia. With this volume off the market, integrated refineries around the world face a growing economic incentive to divert VGO (Value Added by Oil) from the base oil train in favor of diesel and jet fuel, whose margins have soared. Competition for the same VGO from higher-netback fuels is one of the most significant drivers of pressure on base oil supply in the medium term.

Natural gas, LNG and the cost of hydrogen

Pearl GTL has a single input: gas from the North Field. With the shutdown of Qatar Energy — responsible for ~20% of global LNG trade — gas prices in Europe practically doubled in 48 hours (TTF: from €31 to >€56/MWh). The impact goes beyond Pearl: Group II and III refineries that produce hydrogen via steam reforming of natural gas (SMR) are facing higher H2 costs, putting pressure on the operational cost of each ton produced worldwide — even in operationally safe plants.

Freight, bunker fuel, and emergency fuel surcharges

Bunker fuel (VLSFO) at the world’s 20 largest bunkering ports reached US$1,017/ton on March 18, according to Ship & Bunker data—almost double the US$544/ton recorded on February 27, the day before the attacks. In Singapore, the world’s largest bunkering hub, VLSFO rose 106%. War insurance premiums for tankers more than tripled. In response, the world’s largest shipping companies implemented Emergency Fuel Surcharges (EFS): Maersk announced an EBS (Emergency Bunker Surcharge) of US$200/TEU on head haul routes, effective from March 25; CMA CGM implemented an EBS of US$150/TEU; MSC announced values of US$60 to US$190/TEU depending on the route. Hapag-Lloyd and ONE followed with similar surcharges, effective from March 23. For base oil cargoes in tankers — the dominant import method for Brazil — the impact is proportional to the freight cost, which is also on the rise. Alternative routes via the Cape of Good Hope add 10 to 15 days of navigation and corresponding chartering costs.

Impact on CFR prices in Brazil

Brazilian Group III CFR prices rose by more than US$400/ton in the week of March 10-14 (USD115/ton on March 19, 2026). Crude oil, VGO, H2, bunker fuel, and EFS have not yet fully been reflected in futures contracts. This movement is dragging down GI, GII, and PAO – all formulators are simultaneously seeking alternatives, and demand for sources outside the epicenter has exploded.

Baseline scenario vs. Disruption scenario

The baseline scenario remains a conflict of limited duration, with a gradual normalization of transit through the Strait of Hormuz within a few weeks. The Strait has never been completely and permanently closed. Every actor in the Gulf—including, in theory, Iran itself—has structural reasons to avoid this outcome.

Goldman Sachs, on March 3, based its projection on just five additional days of very low exports via Hormuz, followed by a gradual recovery over the course of a month. The IEA released 400 million barrels from strategic reserves — the largest operation in its 50-year history. On March 15, Iran’s Foreign Minister told CBS News that Tehran is open to negotiations on safe passage. Prices temporarily retreated after news of possible contact between the two countries.

The disruption scenario materializes after 60–90 days without resolution: feedstock from Korean refineries depleted; global GIII capacity cuts announced; Pearl GTL and Ruwais still grounded; GIII availability on the spot market — SK-Pertamina, PETRONAS Melaka, SK Enmove Cartagena — insufficient to cover global demand, with some of these volumes restricted by OEM approvals for premium grades.

What to do: a guide for Brazilian formulators

Brazil imports 100% of its Group III crude oil. Primary sources are all in a high to critical risk zone. The increase of over US$400/t already recorded is real and needs to be immediately incorporated into procurement costs. The response must be structured across two distinct timeframes.

Short Term — Next 30 to 60 Days

Confirm stock level

Map the current Group III inventory and calculate how many days of production it covers. The minimum target is 60 days. Those below this need to act before available volumes become even scarcer and more expensive.

Activate alternative, lower-risk sources.

SK-Pertamina (Dumai, Indonesia) and PETRONAS Lubricants (Melaka, Malaysia) are the sources with the best combination of low geopolitical risk, proven quality, and some relevant volume. Immediate contact for spot availability and short-term contracts is the number one priority—with the understanding that the Asian market is also very short of GIII and will compete for these volumes.

Pricing the real cost already

Part of the cost increase hasn’t yet reached invoices because existing contracts were signed before the war. The adjustment will come in the next remittances—including EFS that begin to take effect from March 23–25. Formulators who don’t pass this on to their clients now will absorb negative margins in the coming weeks.

Don’t panic buy

Emergency and disorganized purchases create artificial shortages and inflate prices even further. The inventory strategy should be based on actual 60-day coverage—not on speculation about how long the conflict will last.

Medium and Long Term — 3 to 18 Months

The conflict, whatever its duration, revealed a structural vulnerability that will not disappear when the Strait of Hormuz reopens. The geographic concentration of global Group III lubricant supply—the Middle East and South Korea accounting for more than 60%—is an inherent risk to the Brazilian lubricant industry. The current window of opportunity presents a chance to address it.

Ongoing supplier diversifications

SK-Pertamina and PETRONAS must migrate from emergency alternatives to regular supply contracts — even with a possible freight premium. Redundancy has a cost. The cost of not having it has become evident in the last three weeks.

China: Prepare, don’t tell.

China was not a relevant alternative before the conflict and is not now. In the medium to long term, if export quotas are expanded and the blockade is lifted with the end of the crisis, Chinese installed capacity represents the largest global volume reservoir. Formulators should use the current period to map suppliers and qualify grades for non-OEM-critical applications—greases, industrial lubricants, off-road transmissions, marine and agricultural applications—so that, when and if that window opens, activation is rapid. The permanent caveat is the limited coverage of OEM approvals for premium grades.

PAO (Group IV) as a strategic complement

Historically, PAO was much more expensive than Group III — around US$2,775/t (PAO 4cSt, USA, Dec/2025) versus US$1,200–1,400/t for GIII. With GIII CFR Brazil already above US$400/t, the price difference has narrowed. PAO has real technical advantages: superior low-temperature performance, greater oxidation resistance, lower Noack volatility — properties that allow for longer drain intervals and lower viscosity formulations, reducing the total volume of base oil per liter of product. For premium PCMO, next-generation automatic transmission fluids, and high-speed greases, PAO becomes economically defensible. Suppliers accessible to Brazil include: ExxonMobil (SpectraSyn), Chevron Phillips Chemical (Synfluid), INEOS, and Idemitsu.

Conclusion: Optionality as a competitive advantage

High-intensity supply chain crises are not anomalies. They are recurrences with unpredictable intervals. The COVID-19 pandemic demonstrated this undeniably in 2020 and 2021: companies that had built “optimized” supply chains for minimum cost discovered, in the most painful way possible, that efficiency without redundancy is fragility disguised as competitiveness. The 2026 war in Iran repeats the lesson — this time in the specific segment of base oils, with an aggravating factor: the geographic concentration of Group III is even more extreme than that of Group II or Group I, and Brazilian dependence is total, without a single local plant as a buffer.

The good news — and it exists — is that the Brazilian lubricants sector now has a window of clarity that did not exist before. Vulnerabilities are mapped, alternatives are identified, and cost drivers are visible. This has value. During the pandemic, many companies operated blindly when the chains broke down.

The central concept that emerges from this crisis is that of optionality. In finance, an option has value precisely because it guarantees its holder the possibility of acting when circumstances are favorable — without the obligation to do so when they are not. In supply chain management, the logic is identical: having a second qualified supplier, even if never activated on a daily basis, is not an idle cost — it is a resilience asset with value that only fully manifests itself in times of disruption. Companies that built this optionality before the COVID pandemic came out ahead when supply chains broke down. Companies that build this optionality now will be in a significantly better position in the next crisis, whether it is geopolitical, logistical or climatic.

The global Group III market will normalize. The Strait of Hormuz will reopen. Middle Eastern plants will resume operations. Prices will retreat from current peaks. This is almost certain — the question is the time horizon and the ability of each company to get through this period without supply disruption and without absorbing margin losses that should have been avoided. The right time to build supply chain resilience isn’t during a crisis—it’s before. For those who haven’t started yet, the second best time is now.

ABOUT FACTORK

FactorK is a strategic consulting firm based in São Paulo, with 28 years of sector expertise in Latin America, operating in Energy & Mobility, Health & Pharmaceuticals, Chemicals & Materials, and Beauty & Wellness. The company combines deep market knowledge with rigorous advisory methodology, research, and digital strategy.

In the lubricants sector, FactorK works with manufacturers, distributors, and buyers of base oils across the entire complexity of the supply chain — from feedstock cost structure and mapping of alternative suppliers to sourcing strategies in geopolitical pressure scenarios and evaluation of alternative base oils. The current disruption in the supply of Group III is exactly the type of problem that requires sector depth and analytical rigor to be navigated without overreaction — and without underreaction.

More information: www.factorkconsulting.com.br

By: Sérgio Rebêlo, Managing Partner at FactorK, holding a degree in Business Administration from EAESP-FGV, an MBA from EAESP/FGV, and a One MBA from Kenan-Flagler Business School (University of North Carolina), EGADE, Erasmus School of Business, and The Chinese University of Hong Kong.

{kind=link}