Lubes em Foco Magazine – issue 97

Click on the magazine and read, download, or share the articles:

It’s already a trademark of Lubes em Foco magazine to research and present its readers with a complete analysis of the Brazilian lubricant market figures, showing the year-end results and the percentage change compared to the previous year. This was also done for the year 2025. Working with market data, researching with the ANP (National Agency of Petroleum, Natural Gas and Biofuels) and the largest companies in the sector, was a challenging task, but one we are already quite familiar with. However, this time we encountered some unusual and more complex situations when we needed to establish a correlation with the year 2024 to determine the market trend.

New ANP code table requires retroactive adjustments.

It turns out that in 2024, the ANP (National Agency of Petroleum, Natural Gas and Biofuels) carried out a revision of the code table, with the aim of reducing the difficulties for companies and increasing the accuracy of the data obtained. Thus, the month of October 2024 was chosen for the implementation of the new codes which, according to the Agency, would considerably reduce the list of products, improving certain classifications, removing the broad scope of the “other” category, preventing some products from being classified under more than one code, and improving the statistical analysis of market figures.

Being also responsible for gathering data related to the Reverse Logistics of Lubricants, which includes collection targets established by Conama Resolution No. 362/2005, and considering that the assessment of these targets is based on the period from October of the year under analysis until September of the following year, it would be only logical for the introduction of the new classification codes to begin in October 2024. Yes, this thinking is correct; however, for those who need to research market figures for the calendar year, i.e., from January to December, the situation has become complex.

Between codes and trends: the challenges of analyzing the market.

Some new codes introduced in October do not have a direct reference to the categories reported from January to September. The new market figures became more accurate, but there was a need to temporarily sacrifice the market trend view, as the numerical variation of each category cannot be so clear. In addition, there were many initial questions from companies, with several requests for data reprocessing, causing retroactive changes throughout the year, even after their publication, causing the past to be modified, bringing a new reality to the present.

Faced with this challenge, we delved deeply into the 2024 figures, understanding their changes and establishing correlations between the oil categories and their variations over time, considering the 12 months of the year in question. The result can be considered successful and, in this context, we publish in this edition the final figures of our research for 2025, which we now present.

A new perspective on 2025

First, it’s important to remember that the figures we will use in this and subsequent analyses will no longer consider the categories of insulating oils and agricultural spraying oils, as well as any other type of base oil and its applications in industry (process, extenders, and plasticizers). Base oils will be analyzed separately from the Brazilian market for finished lubricants.

The result of the Lubes in Focus analysis, considering the above, is a 1.6% growth in the Brazilian lubricant market, reaching a total of 1,524,596 m3 of finished lubricating oils.

To validate this number as a low, yet consistent, market growth, we can observe some national parameters and their variations, which are closely linked to the lubricant market. These include the Industrial GDP, which showed a growth of 1.4%, automotive sales with an increase of 2.1%, and the consumption of liquid fuels, which rose 2.7%, all in comparison to the year 2024.

To validate this number as a low, yet consistent, market growth, we can observe some national parameters and their variations, which are closely linked to the lubricant market. These include the Industrial GDP, which showed a growth of 1.4%, automotive sales with an increase of 2.1%, and the consumption of liquid fuels, which rose 2.7%, all in comparison to the year 2024.

Market share – Year 2025

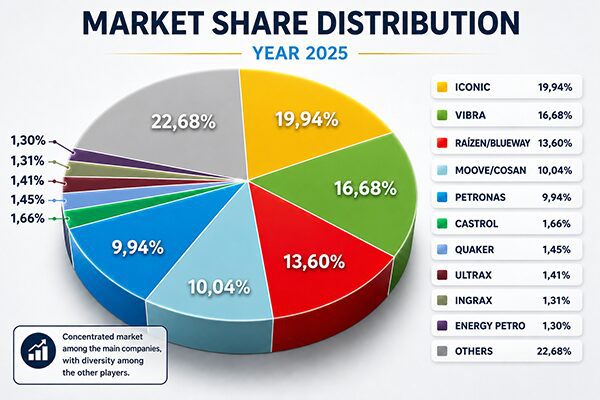

Maintaining tradition, the five largest distributors (TOP 5) held just over seventy percent of the Brazilian lubricant market. Iconic continued to lead the market with almost 20% market share, followed by Vibra, Blueway (Raízen), Moove, Petronas, Castrol, Quaker, Ultrax, Ingrax, Energy Petro and others (22.68%). In this context, we need to take into account the temporary shutdown of Moove in early 2025 due to a fire at its facilities, and the impressive speed in resuming operations, which still allowed it to secure fourth position.

Maintaining tradition, the five largest distributors (TOP 5) held just over seventy percent of the Brazilian lubricant market. Iconic continued to lead the market with almost 20% market share, followed by Vibra, Blueway (Raízen), Moove, Petronas, Castrol, Quaker, Ultrax, Ingrax, Energy Petro and others (22.68%). In this context, we need to take into account the temporary shutdown of Moove in early 2025 due to a fire at its facilities, and the impressive speed in resuming operations, which still allowed it to secure fourth position.

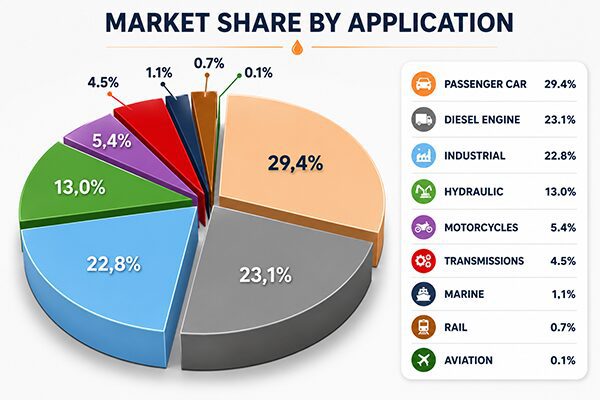

Looking at the market considering the main applications of lubricants, we find oils for Otto cycle engines leading with 29.4%, followed by oils for diesel engines with 23.1%, general industrial oils with 22.8%, hydraulic oils with 13.0%, etc., as shown in the graph. It is worth noting that in the industrial classification we are grouping together applications for chainsaw chains, gears and circulating systems, hydraulic oils, multi-purpose applications, textiles, metalworking, and other industrial applications.

Looking at the market considering the main applications of lubricants, we find oils for Otto cycle engines leading with 29.4%, followed by oils for diesel engines with 23.1%, general industrial oils with 22.8%, hydraulic oils with 13.0%, etc., as shown in the graph. It is worth noting that in the industrial classification we are grouping together applications for chainsaw chains, gears and circulating systems, hydraulic oils, multi-purpose applications, textiles, metalworking, and other industrial applications.

Foreign market: Exports and Imports

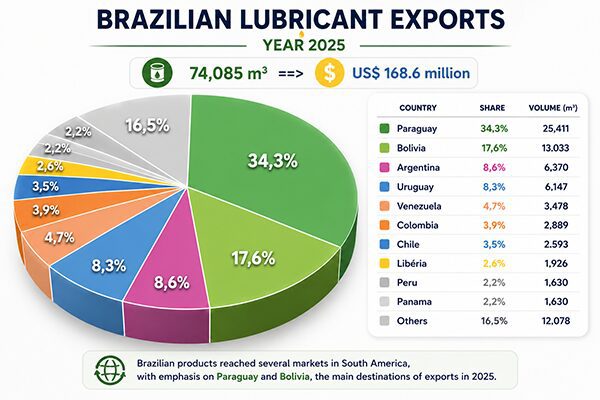

In 2025, Brazil exported 74,085 m³ of finished lubricating oils, generating foreign exchange earnings of approximately US$168.6 million. The main destinations were Paraguay, responsible for 34.3% of exports, followed by Bolivia, Argentina, Uruguay, Venezuela, Colombia, Chile, Liberia, Peru, Panama, and other smaller countries.

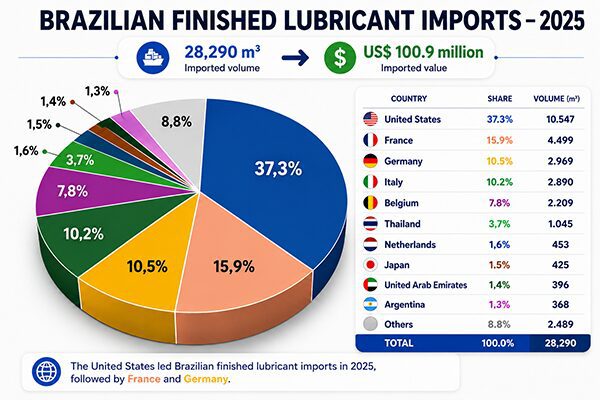

Imports totaled 28,290 m³, with US$100.9 million sent abroad. The United States was the main partner, accounting for 37.3%, followed by France, Germany, Italy, Belgium, and others, as shown in the graph.

Imports totaled 28,290 m³, with US$100.9 million sent abroad. The United States was the main partner, accounting for 37.3%, followed by France, Germany, Italy, Belgium, and others, as shown in the graph.

Base oils

Base oils

The total market for base oils traded in Brazil reached a volume of 1,705,614 m3 in 2025. Of this amount, 26,123 m3 were destined for export, leaving 1,679,491 m3 for the Brazilian market.

Brazilian refineries produced approximately 620,260 m3, corresponding to 36.4% of the total market. REDUC, located in Rio de Janeiro, was responsible for 81.6% of this production, with 506,511 m3 of Group I base oils. LUBNOR, in Ceará, producing naphthenics, accounted for 10.2%, and the Mataripe Refinery in Bahia, for 8.2%. Meanwhile, the rerefining industry contributed 333,884 m3, representing 19.6% of the market.

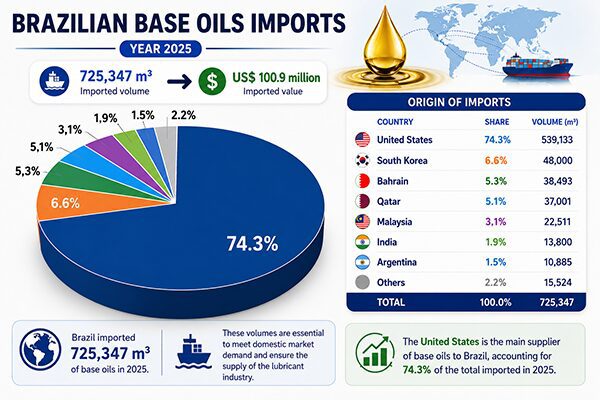

Brazilian imports of base oils totaled 751,469 m3, representing 44.1% of the total market. Compared to the previous year, this volume decreased by 6%, however, we must consider that 2024 was the second largest import volume in history, second only to 2021, which was the recovery after the pandemic. Brazil thus spent a total of US$489 million in 2025, considering freight and insurance, i.e., the CIF price.

The United States was once again the major supplier of base oils to Brazil, accounting for 74.3% of Brazilian imports, followed by South Korea with 6.6%, Bahrain with 5.3%, Qatar with 5.1%, Malaysia with 3.1%, India with 1.9%, Argentina with 1.5%, and other smaller countries that totaled 2.2%.

The outlook for the Brazilian lubricants market in 2026 could be considered good, in line with expectations from the automotive industry, agribusiness, and industry as a whole. However, global geopolitics has presented critical and sensitive aspects that could cause disruptive events to impact prices and supply sources, significantly altering initial projections. As we write this article, the world is witnessing wars, supply restrictions, soaring prices, and other unpredictable factors that radically change the course of events. Inflation is another parameter that hinders efficiency and the appetite for investment. In these times, caution dictates that the industry should prepare with safety stocks, avoid debt, and conduct meticulous monitoring to devise the best strategies for its businesses. In the lubricants segment, Lubes em Foco magazine will always keep a watchful eye on bringing the best information about technologies and market changes to keep its readers updated.

{kind=link}