Por: Amanda Hay (Deputy Managing Editor, Americas at ICIS)

Por: Amanda Hay (Deputy Managing Editor, Americas at ICIS)

Leia em Português

Lea en español/castellano

Force majeure for base oils was inevitable

Force majeure for base oils – US base oil inventories remain too low to adequately supply key export markets that rely on the US for material.

Supplies for export are expected to be tight for the majority of 2021, which will have significant effect for South America.

ICIS estimates that the region sources 85% of its base oil supply shortfall from the US.

Replenishing stocks is the immediate goal

Base oil buyers in South America have had to turn to other regions for material, which is globally short, and have found sourcing material to be extremely difficult.

US producers are focused on rebuilding their stocks following the February polar storm and preparing for an active Atlantic hurricane season. They did not have sufficient stocks before the storm.

The producers are honoring their contractual obligations, but very little material is being sold outside of term contracts.

The polar storm shut down 42% (89,200 bbl/day) of total US virgin production capacity, according to ICIS data, by affecting four major refineries: Motiva (Port Arthur, Texas), ExxonMobil (Baytown, Texas), HollyFrontier (Tulsa, Oklahoma) and Calumet (Shreveport, Louisiana).

Groups I and II were the most affected

The impacts were larger when looking at specific groups. The storm affected 41% of Group I production capacity and 38% of Group II production capacity.

Motiva and ExxonMobil were unplanned shutdowns, while HollyFrontier and Calumet were prolonged turnarounds.

Both Motiva and ExxonMobil declared force majeure. They have resumed their operations, and ExxonMobil has lifted FM on Group I but not Group II. Supplies are improving gradually from both refineries.

HollyFrontier and Calumet were undergoing planned maintenance, but the storm caused problems that needed extra repairs and delayed the restarts. HollyFrontier was down about a month longer than planned, and Calumet was down at least two weeks longer than planned.

Offer will remain restricted until the fourth quarter

While production rates continue to improve, supply is critically tight. Refiners cannot catch up to demand and are keeping volumes for the domestic market while they recover.

Brightstock is the tightest grade, followed by heavy neutrals and mid neutrals. Europe has noted an increase in demand for material from South America, but the region expects volumes available for export to be short until the fourth quarter. Planned maintenance in Europe adds to tightness.

Buyers in South America must adjust to the challenges of a limited number of offers available and at rising prices.

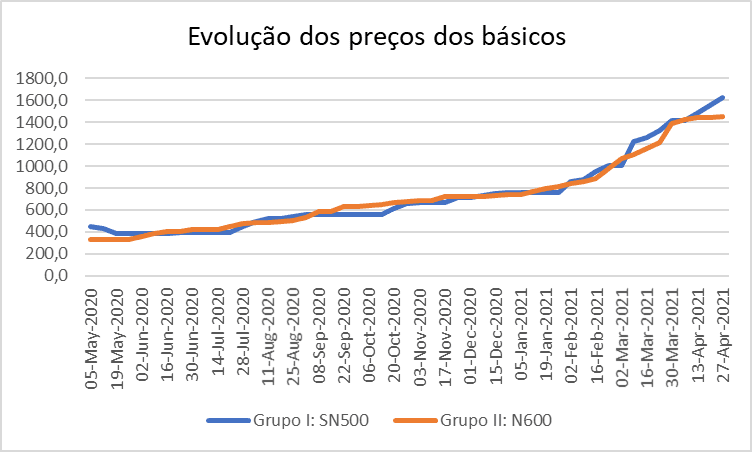

US export prices for Group II N600 and Europe prices for Group I SN500 are more than four times the low points reached in the pandemic.

“Availability is an issue,” a market player said, regardless of volume.

“There are no questions on price,” another participant said.

“Blenders may buy finished product rather than base oils,” a market player said, although production rates of finished product are affected by base oil and additive shortages.

There is an expectation that it will take until after hurricane season to rebalance supplies in the US.

Prices in the last 12 months

Blue line: Base Oils Paraffinic SN500 FOB Europe Assessment Export Spot 2-4 Weeks Full Market Range Weekly (Mid) : USD/tonne

Blue line: Base Oils Paraffinic SN500 FOB Europe Assessment Export Spot 2-4 Weeks Full Market Range Weekly (Mid) : USD/tonne

Orange line Base Oils Paraffinic Group II N600 FOB USG Assessment Export Spot 2-6 Weeks Full Market Range Weekly (Mid) : USD/tonne

#portallubes #lubricants #greases #cars #automobiles #motorcycles #trucks

{kind=link}